Q1 Shockwaves: From Optimism to Uncertainty

The first quarter reminded us how quickly market leadership and sentiment can shift. What started as a year anchored by optimism around rate cuts and continued AI momentum quickly turned into a far more uncertain environment. The escalation of the Iran conflict, combined with a sharp surge in oil prices, forced investors to reassess both inflation expectations and the path of monetary policy.

U.S. Equities: Mega-Cap Tech Retreat, Defensives Rise

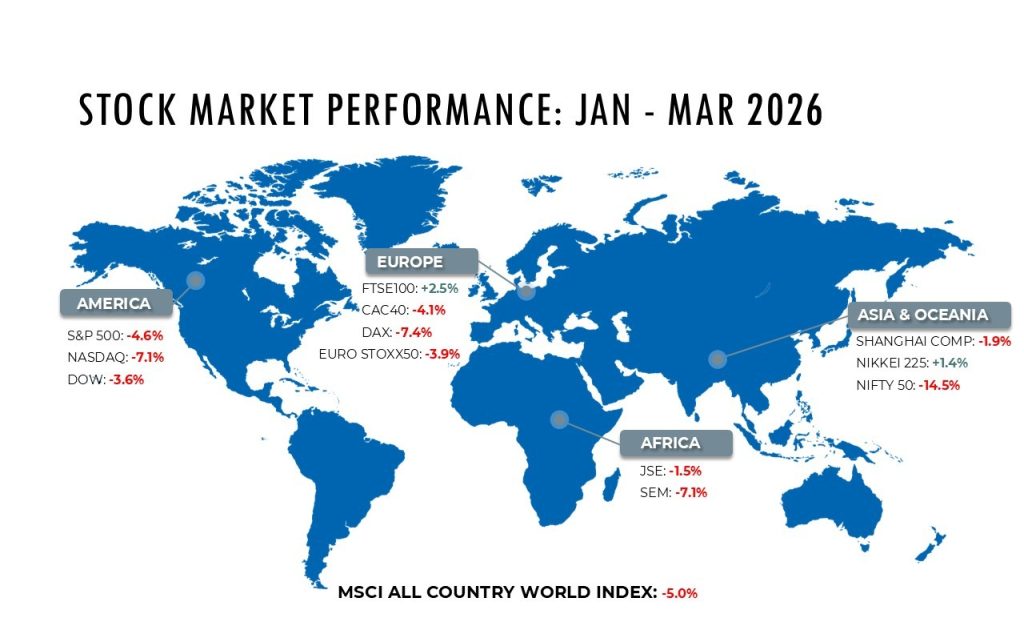

In the U.S., markets underwent a clear rotation away from mega-cap tech into defensive and value sectors. Energy and consumer staples benefited from higher oil prices and safe-haven flows, while AI-driven stocks saw momentum slow amid valuation concerns. Financials also faced pressure as geopolitical risks led to more cautious lending and capital allocation.

US equities enter the next quarter at a crossroads, with markets trading below fair value but facing significant macro and geopolitical headwinds. Mega-cap tech and AI have been repriced, while energy and defensive sectors benefit from elevated oil prices and the U.S.–Iran conflict. Investors are likely to remain selective, favoring resilient, cash-generative companies, with volatility expected to stay elevated and a defensive, tactical allocation approach prevailing.

European Markets: Volatility Persists

European equity markets were pressured in Q1 as Middle East tensions drove volatility and higher energy prices, leading to declines in major indices such as the STOXX 600 and Germany’s DAX, while the UK’s FTSE 100 showed relative resilience due to its energy and commodity exposure. Rising oil prices and inflation concerns weighed on sentiment, with energy stocks among the few outperformers, while growth-sensitive sectors underperformed amid higher input costs and slowing economic expectations. Overall, Europe lagged U.S. equities, with performance driven by energy price dynamics, currency movements, and increased risk-off positioning.

European equities are expected to remain volatile in the coming quarter, with valuations around fair value and limited upside, as elevated oil and gas prices driven by the U.S.–Iran conflict continue to pressure corporate margins and consumer demand. Defensive sectors, energy, and defence may outperform, while cyclicals face pressure. Selective positioning in high-quality, cash-generative, and globally exposed companies is preffered.

Japan: Nikkei Rallies on Yen Weakness, Shields Risk

Japan was a standout in the first quarter despite broader risk‑off sentiment. The Nikkei 225 outperformed major equity indices, supported by a weaker yen, continued policy support, and improving trade openness. Export‑oriented and growth stocks led the advance, buoyed by optimism around corporate reforms and stimulus continuity following the ruling party’s strong political position.

The combination of yen depreciation and stable domestic demand helped cushion Japanese equities against global headwinds. While geopolitical tensions weighed on risk appetite, Japan’s market structure allowed it to outperform many developed peers, particularly as value‑oriented sectors garnered renewed attention.

India: Oil Surge and Currency Woes Shake Markets

India’s equity market had a weak first quarter, driven by valuation corrections, rising geopolitical tensions, and a shift to risk-off sentiment. Higher crude prices pressured inflation, the current account, and corporate margins, while FII outflows and a weaker rupee further weighed on markets despite RBI intervention.

Domestic investors offered partial support, but external factors dominated. While near-term risks remain due to energy prices, currency volatility, and foreign outflows, India’s strong domestic demand and structural growth drivers support a cautiously positive medium-term outlook.

Bond Yields Jump on Inflation Concerns

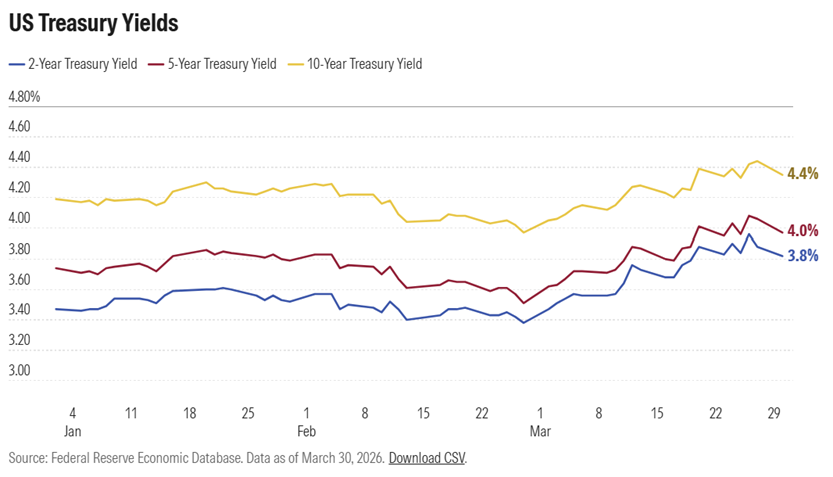

Even before the outbreak of the Iran war, the Fed was navigating a challenging backdrop, with inflation still above the 2% target and signs of a cooling labor market. Expectations had been building for rate cuts in 2026, particularly under the anticipated leadership of Kevin Warsh, despite ongoing political pressure from Donald Trump.

However, the resurgence of inflation risks driven by the conflict has materially shifted market expectations, with forecasts for rate cuts largely fading and bond markets increasingly pricing in the possibility of further tightening. This repricing has pushed yields higher across the curve: the U.S. 10-year Treasury yield has risen from below 4% to around 4.3%, while shorter-term yields have also climbed notably, reflecting a more cautious and hawkish outlook.

European government bonds also declined, down 0.6% over the quarter. The ECB maintained rates in March but clearly indicated a tightening bias. Updated projections point to inflation reaching 3.1% year-on-year by Q2 2026, before fully factoring in recent energy price spikes, suggesting further upward pressure on yields across the region.

UK Gilts were the weakest performers of the quarter, falling 2.0% after a volatile period. Earlier strength reversed following the Middle East–driven energy shock, which exposed the UK’s reliance on natural gas and heightened inflation risks. In response, the BoE adopted a more hawkish stance in March, signalling a readiness to tighten policy if needed. The unanimous decision to hold rates, alongside even dovish members hinting at possible hikes, reinforced upward pressure on Gilt yields.

Japanese Government Bonds declined 1.6% over the quarter, with longer-dated yields rising sharply ahead of February’s snap election as markets priced in expectations of looser fiscal policy under Prime Minister Sanae Takaichi. At its March meeting, the BoJ signalled a willingness to tighten policy in the near term, highlighting greater concern over upside inflation risks than potential downside growth impacts from the energy shock.

Oil: Historic Surge Amid Middle East Tensions

Oil markets saw one of the most extreme moves in recent history, with Brent up 94.5% and WTI 76.6%, climbing from early-year lows near $60 to over $100 by late March. The escalation of the U.S.–Iran conflict, including military strikes and the effective closure of the Strait of Hormuz, triggered a severe supply shock. Damage to LNG and industrial infrastructure amplified the impact across broader commodity markets.

Near-term trading is expected to remain volatile between $90–$110/bbl, with potential for spikes toward $120–$150 if disruptions persist or sharp retracements to $70–$75 if diplomatic progress is made. Oil dynamics continue to influence central bank expectations, corporate margins, and broader risk sentiment globally.

Precious Metals: Gold and Silver Rollercoaster

Precious metals experienced sharp swings, with gold rising 8.3% and silver 5.4%, masking significant intra-quarter volatility. Both metals surged in January, before retreating as rising bond yields and a stronger U.S. dollar offset traditional safe-haven demand. Silver’s industrial usage amplified its sensitivity to risk-off moves.

Structural demand remains supported by central bank purchases, geopolitical fragmentation, and a diversification push away from fiat currencies. Short-term performance will continue to track oil prices and central bank policy: easing Middle East tensions could support gold toward $5,000+, while sustained inflation pressures could weigh it down toward $4,500–$4,000.

U.S. Dollar: Safe-Haven Strength

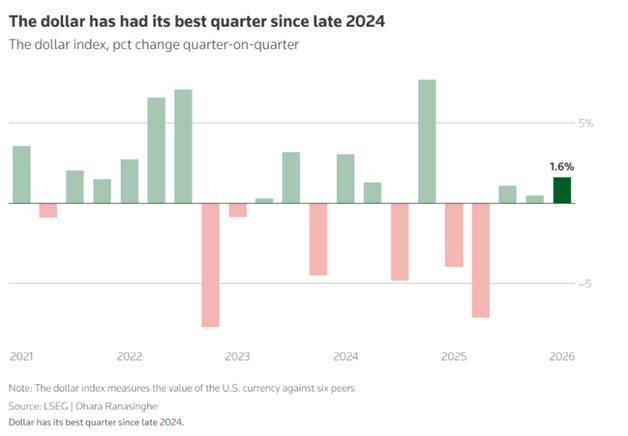

The U.S. dollar strengthened 1.7% in Q1 2026, reflecting risk-off flows and the U.S.’s relative advantage as a net energy exporter. Rising oil prices and geopolitical uncertainty fueled capital inflows into dollar-denominated assets, reinforcing its role as the global reserve currency.

The trajectory of the dollar depends on the conflict’s duration. A short-lived escalation may allow modest dollar easing, while prolonged tension could sustain dollar strength, particularly versus the euro and yen. Emerging market currencies remain under pressure, with macro and geopolitical risks continuing to drive safe-haven positioning.

Cryptocurrencies: Macro Pressures Trigger Sharp Declines

Cryptocurrency markets faced significant pressure, with Bitcoin down 22.1% and Ethereum falling 29.2%, marking one of the weakest quarterly starts in recent history. The selloff was driven by the U.S.–Iran conflict, hawkish U.S. monetary policy, and persistent ETF outflows, creating a broad risk-off environment.

By March, signs of stabilization emerged as prior deleveraging reduced forced liquidation risk. Bitcoin showed relative resilience compared with other asset classes, while Ethereum remained highly sensitive to risk sentiment, amplifying volatility. Going forward, crypto performance will remain closely tied to geopolitical developments, energy market trends, and global liquidity conditions. Recovery is possible if tensions ease and macro risks moderate, but downside risks persist in the near term.

Looking Ahead

Markets enter the next quarter with elevated uncertainty, shaped by geopolitical tensions, high oil prices, and inflation pressures. Elevated oil and ongoing Middle East risks are expected to influence central bank guidance, risk sentiment, and asset allocations across equities, bonds, and currencies. Investors are likely to remain selective, favoring companies with resilient earnings, strong balance sheets, and structural growth, while defensive and energy-linked sectors may continue to outperform. Volatility is expected to stay elevated, underscoring the importance of tactical and cautious positioning.

- investment@providentiamanagers.com

- (+230) 5941 9878